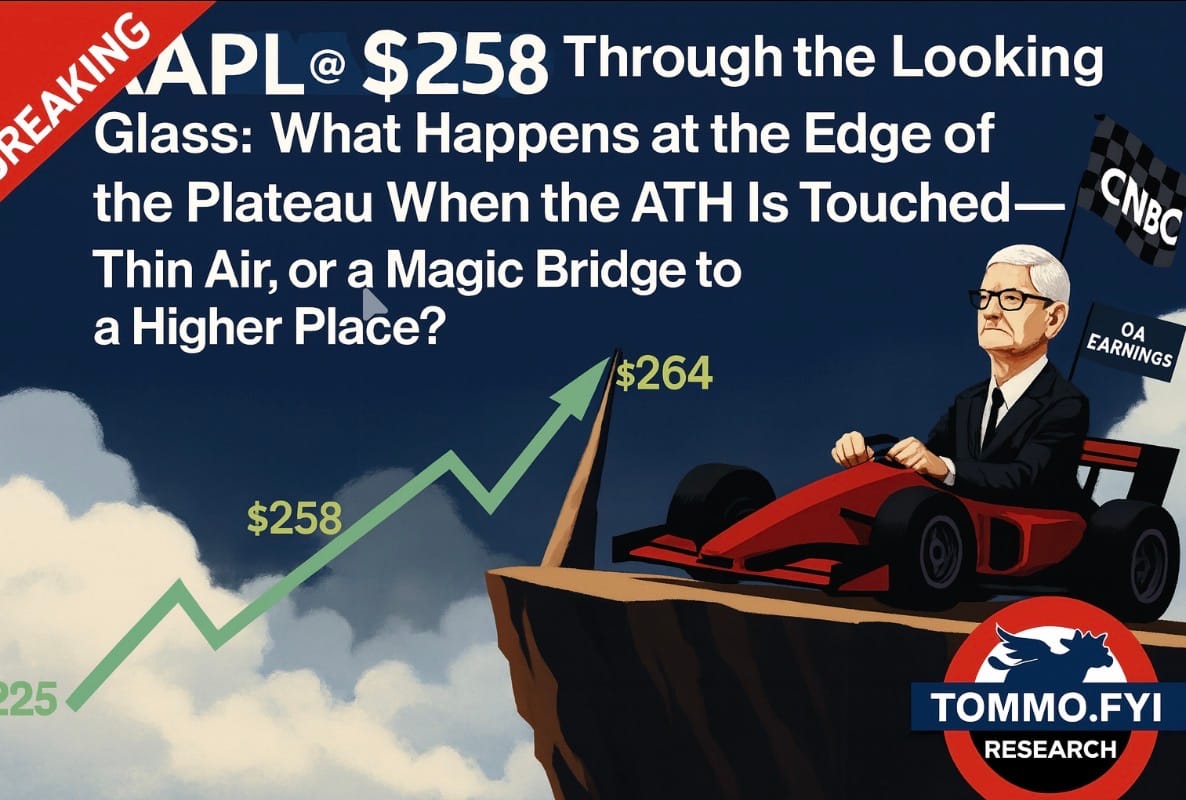

AAPL takes out its ATH $263. Would I be a seller here (again)? Yes. Too far, too fast, no clarity.

Markets are at a precipice of the traditional strong end of year, but has that already been spent in the enormous run-up since the April? Four charts, one long-form commentary: I believe in booking gains, pocketing cash, and being able to buy dips. “You don’t have to sell out, just raise some cash.”

A couple of weeks ago it was euphoria. I said I’d sell when the stock hit $258.

TL;DR 10 Key Takeaways from today’s action

- AAPL has blown off above $260 for the second time this year — repeating its February–March pattern before dropping $15–20.

- Today’s rally is narrative-driven, not earnings-driven — sustained almost entirely by analyst upgrades citing “iPhone 17 demand.”

- Those upgrades are benchmarked against a weak 2024 (iPhone 16) cycle, making “record growth” statistically meaningless.

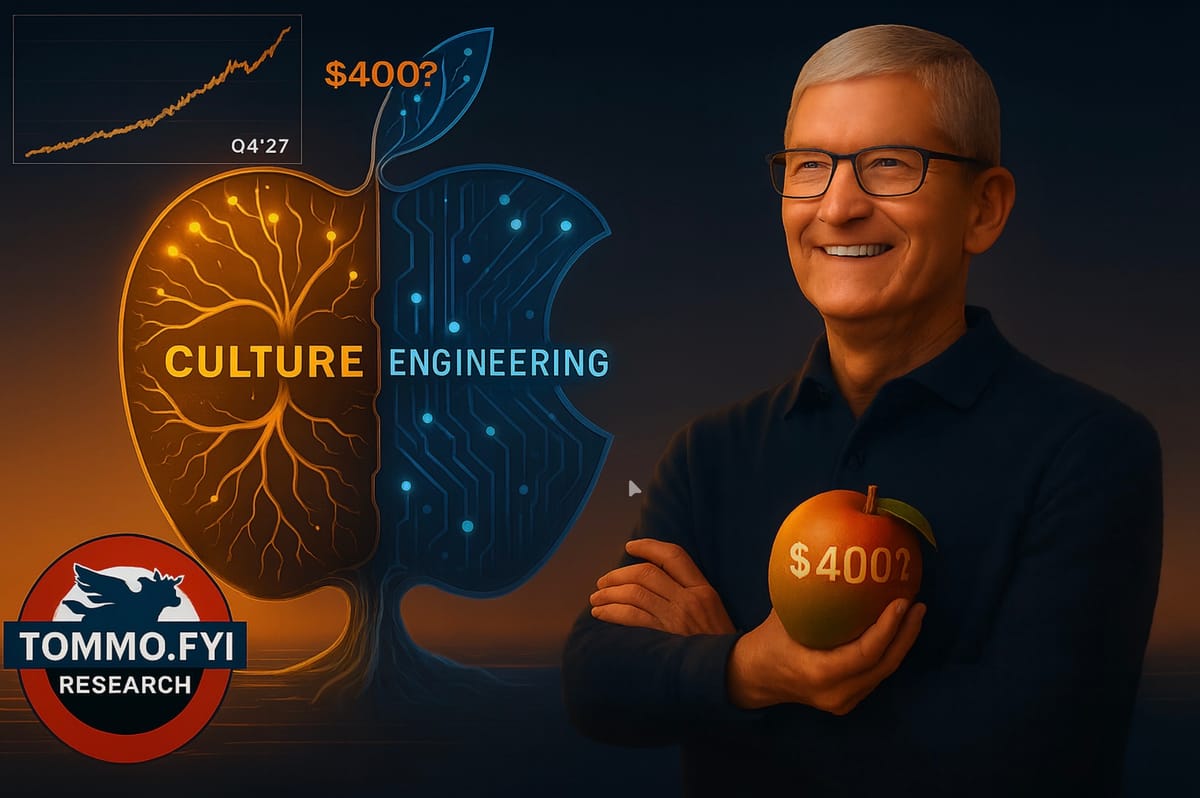

- Institutional desks are front-running the buyback, not fundamental growth — Tim Cook’s financial engineering has replaced innovation as the earnings driver.

- AI and Siri delays are still the elephant in the spaceship. The real “intelligence gap” isn’t technical; it’s cultural and managerial.

- Apple’s top-talent drain continues — those leaving cite control, secrecy, and lack of creative autonomy, not just compensation.

- Valuation is detached from innovation reality: 39× earnings for low-single-digit growth is unsustainable once buyback effects fade.

- Retail investors are mistaking motion for momentum — a dopamine rally amplified by “ATH” headlines and algo trading.

- Q4 could be saved only through a “Financial Escape from Alcatraz” — boosted by buybacks, AppleCare margins, and deferred tax magic.

- I’m not short — I’m sane. I’d sell half here, hold cash, and re-buy the dip under $245. It’s not timing; it’s intelligent rotation.

This isn’t a hit piece.

It’s a sanity check on a stock priced for reinvention, without any reinvention yet delivered. So please read the notice below before reading any further:

For anyone worrying, I’m sure “those nefarious options traders” people like to blame for driving AAPL investors to “Max Pain” are already at it, and someone will be blaming Apple’s supposed inability to buy its own stock during a mis-termed “blackout period” for today’s air pocket - so don’t worry:

It’ll all be over by Monday 27th October, and the roller coaster will be back underway as calls to “buy the dip” echo down the street and across the forums. But.. today is another example that hot air and hopium is underpinning markets, NOT fundamentals.

And if you don’t read anything else in this article, keep that one comment in mind.

So, at the last test of the ATH, AAPL promptly fell from $258 to $245 over two days:

This morning, October 22nd, here was the long term picture : $263 and investors patting themselves on the back for being right (a year on from when AAPL last his $260):

Or viewed longer term (long term, these days, being a month):

Subscribe for free by accepting early Founder Member access to this tier — and early beta access the moment it goes live.

Does this look sane or sensible to you, or a lot of hot air blowing out of the vapour chamber?

For those who don’t know, I publicly sold out around $260 in December 2024. I did two great trades in February and March.

Now, nothing would make me buy AAPL again until they prove they can execute, not just iterate, after their Siri and AI fiasco, and the lies which accompanied it.

Today, I would have sold half over the $260 crest again, raised cash, and waited for a (hopeful) pullback and re-bought my 50% at a discount, booking some handy profits. That’s how you avoid having to sell your AAPL every year to raise cash - just do some trading around your core position.

That’s how you accumulate on “buy the dip” while not sacrificing your trajectory.

Investing is not a zero sum game. You don’t have to “trade” - just reallocate cash to ensure you can maximise returns. That’s not trading, it’s called allocation. Or in farmer terms, crop rotation and watching the weather.

TODAY: From $263 to $254 quicker that you can say “Amit @ EverOptimistic Analysts” says BUY the iPhone 16 YoY comparable growth story.”

The crowd now calling Apple’s latest iPhone 17 “sales surge” incredible are the same ones who described the 16’s catastrophic launch as a “temporary pause.”

If your baseline is a crater, then yes, any movement upward looks like Everest. Analysts are collectively grading on a curve so steep it bends the market back on itself.

💡 And now the same crowd who cheerled the rise, are wailing that the iPhone Air is a flop in China, and everyone should sell. But… we knew that already, because Apple had already increased orders of the Pro and the base 17 having spotted the trend before it emerged, and - efficiently as ever - re-tooled is fabs to change the assembly mix. The delay of the Air in China, was actually a blessing which allowed the company to pivot around my prediction - and its discovery - that this year’s Air is not the phone everyone wants, and is a compromise with a boob tube: until they ditch the “plateau,” this isn’t an Air, but more of a “speed bump” in the road.

I said the same thing the last time we broke above $258:

That this was a blow-off top masquerading as momentum. We got the pullback to $245, then the inevitable re-inflation as the same analysts, suddenly facing price targets about to go underwater, rushed to issue new ones. Not because they’d discovered new data, but because not raising would have been tantamount to telling their clients: “Our Buy rating is under water.”

That’s how you manufacture a rally — with career protection, not conviction.

Meanwhile, Cook’s Apple is doing what it does best:

Perfecting the art of inertia. There’s still no tangible AI strategy, Vision remains a vanity plaything, and the most exciting thing about iPhone 17 is that it’s orange. The company’s narrative machine has now fully overtaken its product engine. Tim Cook’s greatest invention isn’t hardware any more but belief management, which when you don’t actually deliver (Siri, Car, AVP, AI, MacBook with a modem, HomeKit which is commercially viable.. I could go on), will bite you on the ass.

So yes, I sold in December 2024 at $260 to put the record straight. In fact, I sold out of all US holdings in March 2025.

Nothing has changed to make me buy back in. When a company can’t execute beyond iteration, the responsible investor reallocates, not prays. I’d have sold half again above $260, banked the gains, and waited for gravity to do its work. That isn’t “trading”; it’s called risk-aware allocation.

Farmers rotate crops. Investors should too.

Sit in one field long enough and you get soil exhaustion. Will I miss a few percent? Maybe. But I’ve had all my cash, to deploy as I want, for a profit elsewhere, in the meantime, until I am sure AAPL is where I want my money. That’s why you rotate around a core position, because the market doesn’t reward loyalty, only nimbleness.

💡 Unless you have a 20 year time horizon, then like most (real world) farmers, you’ll slowly see your investment eaten by inflation, taxes, opportunity cost elsewhere, because you’re in love with the products, not the company. Love Apple, but don’t give management or AAPL a pass just because you’re invested in it. Their job, is to make you rich. It’s not for you, to give them a pass, for screwing up. That’s not legacy, that’s hubris.

Look at the tape: $263 on Tuesday, $254 on the dip today

A $10 vaporisation on nothing but air escaping from analysts’ helium tanks. The same funds that were chasing the print now scramble for a rationale. “Profit taking,” they say, when what they mean is “panic hedging.”

Apple is not doomed, but it is priced like divinity.

A 40× multiple for 2–3% growth is not valuation! It’s hero worship. And worship always ends in disillusionment. The market isn’t punishing Apple for being bad; it’s punishing investors for pretending it’s still 2012.

I still see a path to $400, and wrote about it yesterday. For those who think I am an AAPL hit-man, I’m just the guy who said BUY for 20 years and wrote about why, and became disillusioned with the company, and its management.

But that doesn’t mean I can’t write negatively about one, while still see the potential in the other. It is not a zero sum game to be hopeful but critical, providing your position has a rationale.

Apple has the competency, but not the culture, to seize the moment. Delay, delay, delay.

But … Apple has to stop lying, delaying and sort out its bloody culture problems, and own its mistakes, the way it used to.

And stop delaying products - it’s just - incompetent.

So yes — at $263, I’m a seller. Again.

Not because I dislike Apple, but because I remember what discipline looks like. The stock will come back. It always does. From 2021-2024 it was the best yo-yo in the market, predictably trading within ranges thanks to no product launches, which made it a traders‘ paradise and investors slow death-by-passive-boredom.

The question is whether the believers will still be able to look at their own charts and admit they’ve been catechised by a corporation.

💡 Because 15-20% YoY growth over the iPhone 16 - if it even is that high, equates to mid-single digit growth when you draw the line back to the iPhone 12, which I did here:.

Before going on to explain why the iPhone 17 launch, had to be viewed through a completely different lens, this year: The flop of last year, incomparable comparables, and an iterative approach to marketing barely upgraded hardware:

And whose chief new feature was no-black-for-you, a terrible UI/UX paradigm in Liquid Glass - which even after 6 months, Apple can’t get right and have had to include a setting to “turn down” in the new beta OS because the interface dynamics simply do not function properly.

Liquid Glass - the UI and UX nobody asked for, nobody likes, and even Apple is admitting just “doesn’t work” and is dialling the entire “effects carousel” down. It looks pretty, until you try to use it, and then all that “glass” and “opaqueness” means you can’t see half the bloody buttons. Opaque, a bit like Apple’s real top line growth.

Reality Check: Don’t Mistake a Blow-Off for a Breakout

Yes, there will be dips, spikes, and the usual theatrical “blow-offs.” That’s Apple’s price choreography these days: the illusion of revelation played in quarterly rhythm. But don’t confuse analysts’ upgrade notes for divine insight. They’re all singing from the same hymnal, built on the same selective comparisons.

Every note you’ve read in the last week touting “incredible iPhone 17 sales” has quietly left out the same crucial clause: relative to last year’s iPhone 16. That’s like applauding a marathoner for beating their personal best after they tripped at mile two the year before. It’s a rebound, not a renaissance.

💡 Context is everything which is why I write at such length, and not in confusing and illogical “analyst note format.” If you can’t be bothered to read more mobiles arguments, why are you even reading this? Just go a read Yahoo News.

Context is exactly what’s missing in these breathless reports.

Ten years of data, ten years of cyclical iPhone seasonality, and yet every note acts as if this one launch is a bolt from the heavens.

💡 The reality: comps are low, excitement is high, and everyone’s pretending that arithmetic equals insight. That’s why I wrote those two articles, to look at history for guidance to the future, which nobody else seems to be bothering to do.

But Apple is still Apple: a master of capital engineering even when product momentum wanes.

When innovation runs out of oxygen, financial alchemy takes over. That’s not cynicism, that’s Cook’s playbook. And if there’s one thing Tim Cook can do better than anyone alive, it’s manufacture calm.

“Escape From Alcatraz: Earnings Season Edition“

Expect the next earnings call to feature what I call “Escape from Alcatraz accounting”: a daring swim through a sea of buybacks, subscription bundling, and “record” AppleCare revenue. It’ll be a triumph of arithmetic over aspiration — a quarter where financial services and insurance reselling patch the holes in the hull. Cook will frame it as “diversification,” the Street will call it “resilience,” and the faithful will nod along, grateful for the illusion of propulsion.

So yes, there will be dips. There will be exuberance. There will even be a few heroic price targets revised up just to avoid embarrassment. But don’t conflate noise with signal, or repetition with truth.

💡 For now, Apple remains a company that can conjure a rally without delivering a revolution, but delaying it, and shedding the very staff tasked with delivering it.

And that, in 2025, is both its genius and its tragedy.

Epilogue: but don’t worry:

Want these updates in short 300-word form in future from the upcoming Live Intraday Dashboard? Sign up now, or if you are a subscriber, make sure your newsletter settings are set to “on”

Turn on your Newsletter Subscription if you’re already signed-up as a member by checking your account settings here:

In the meantime:

“Take Heed of Sharp Turns Ahead. Don’t Ignore The Tell-Tale Signs of Wearing Out at the Edges. Hedge, Don’t Edge, as I’ve Been Warning Since July. Use the VIX”

— Tommo_UK, London. Wednesday, 22nd October 2025.

Any comments, or thoughts, from investors, as opposed to 20-year long buy-and-holders who couldn’t care less because they’re just glad to be living off the dividends from their 11,000% share price increase? Leave them below 😎

X: @tommo_uk | Linkedin: Tommo UK

See the share buttons to LinkedIn, social media and email? Please, use them and help keep .fyi free at the point of readership. Or email this article on to a friend-in-need.